Insights

Plaid just changed the conversation on agentic commerce.

Plaid's ChatGPT move is bigger than fintech product news. The connective tissue for consumer agents is getting real, and insurance carriers should redesign around a buyer who is better informed than ever.

The old moat in consumer finance was not intelligence. It was inertia.

Anish Acharya recently used a phrase that captures a lot of modern financial services better than most strategy decks ever will: profitable apathy.

It is a useful way to understand how a lot of modern financial services still make money.

A surprising number of consumer financial products do not depend on the customer making a bad decision. They depend on the customer not making a decision at all. Or making it too late. Or being too busy to compare. Or giving up halfway through a form. Or accepting the default because the alternative requires paperwork, research, phone calls, and five disconnected systems that do not talk to each other.

That is what made so much of consumer finance durable. Not product excellence. Not always brand. Often just friction.

Which is why Plaid's announcement last week matters far beyond fintech.

On May 15, Plaid said ChatGPT users in the U.S. can now connect financial accounts through Plaid and get real-time answers grounded in their actual financial situation, not generic best practices. Plaid also made the bigger point clearly: the next generation of financial experiences will be built on three things working together at once. Broad data access. Semantic understanding. Trusted permissions.1

That combination is what changes the shape of the market.

What Plaid announced is the beginning of a consumer agent layer in finance.

What changed when Plaid connected ChatGPT to live financial context

For the last two years, most conversations about AI in financial services have been oddly shallow.

The optimistic version was that AI would help consumers understand products better.

The cynical version was that firms would use AI to price more aggressively, target more precisely, and extract more surplus.

Tyler Griffin laid this out well in The Two Paths of AI-Enabled Fintech. One path is AI killing the confusopoly by making complexity legible. The other is AI being used to sharpen discrimination and extraction.2

Both paths are real.

What Plaid did last week is make the first path more operational.

ChatGPT answering a question about money is not new. What is new is the answer being grounded in live financial data, tied to permissions, and connected to whatever comes next. That is where advice starts turning into agency.

A chatbot telling you to save more is forgettable.

A system that sees your cash flow, understands your liabilities, recognizes your income cadence, and can route you toward a relevant next step is something else entirely.

Plaid is starting to look less like connectivity and more like consumer infrastructure

Most people still file Plaid under connectivity. That description is starting to get stale.

The stack now matters more than the connector.

Payroll data can turn a vague insurance question into a real starting point

Plaid's Payroll Income product can instantly verify employment details and gross income information from a connected payroll account, including information available on a pay stub.3

That matters because it changes the starting point.

Take term life.

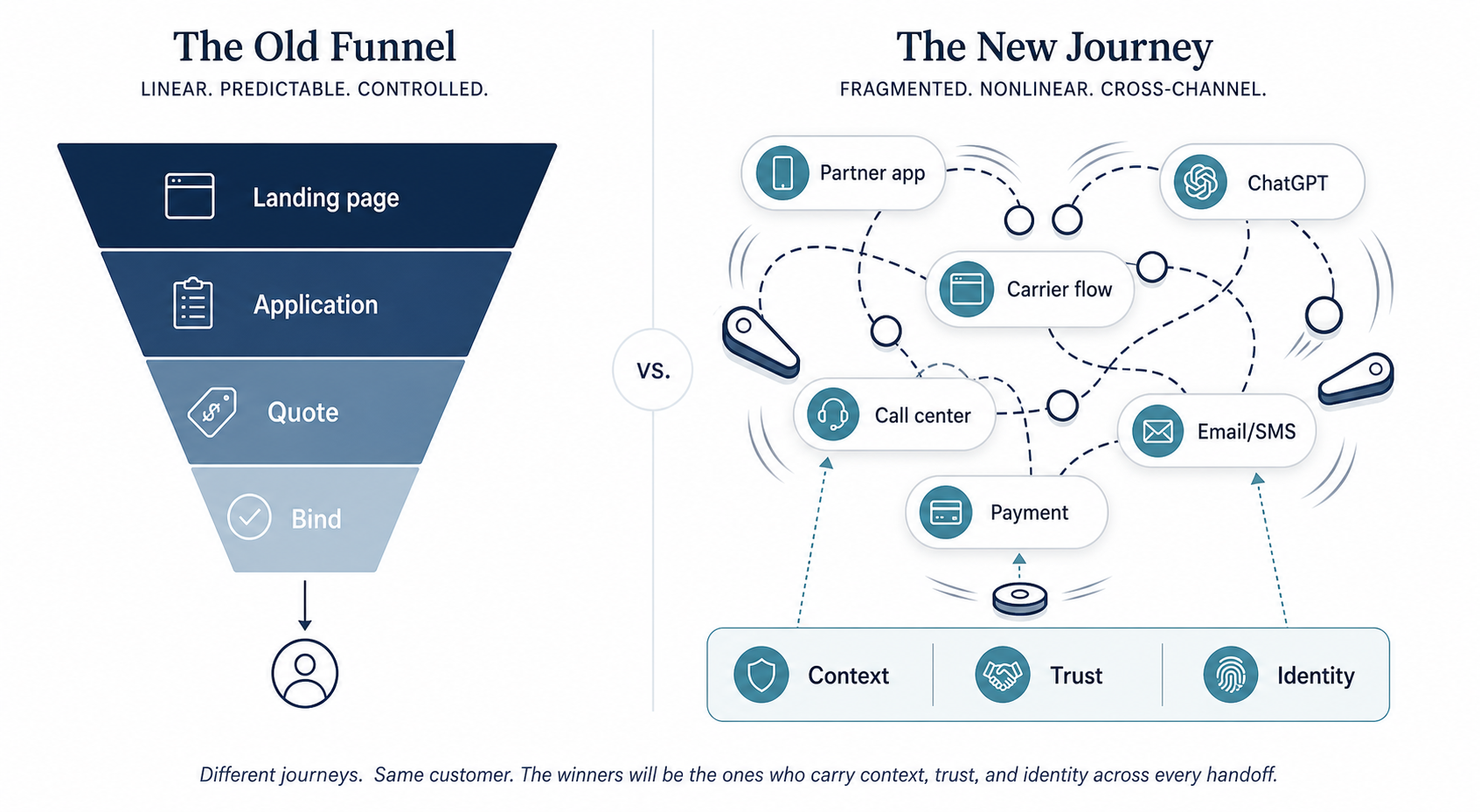

The old consumer journey looks familiar to anyone in insurance: a person vaguely knows they should probably have coverage, postpones it for months, finally Googles around, gets overwhelmed by product choices, maybe fills out one half-baked form, and abandons the process.

The entry point becomes a question instead of a lead form.

“Do I have enough life insurance?”

If the user has already permissioned payroll data, the system is no longer starting from zero. It has verified income and employment context. Add basic household information and suddenly the experience can move from generic education to an informed starting point: rough coverage guidance, relevant term life ranges, prefilled quote entry, and a much tighter handoff into the carrier flow.

Underwriting still exists, of course.

What disappears is a lot of the dead air before the quote.

Transaction data can surface adjacent insurance needs before the customer articulates them

Plaid's Transactions product can retrieve up to 24 months of transaction history and enrich it with merchant identity, category, amount, and related attributes.4

That opens a second category of use cases: inferred need.

Take pet insurance.

If a consumer's transaction history shows recurring Chewy purchases, vet payments, pet pharmacy charges, boarding spend, or grooming activity, the system has a pretty strong signal that this household has a pet. Not because the user filled out a marketing form. Because their real spending behavior says so.

Nobody wants a product that feels like it is stalking them.

But there is a big difference between being pushy and being less blind.

It can prompt at the right moment. It can compare options before the next large vet bill. It can route from recognition to recommendation to transaction with far less waste than the old model of waiting for the customer to self-identify in the right place at the right time.

The customer no longer has to do all the stitching by hand.

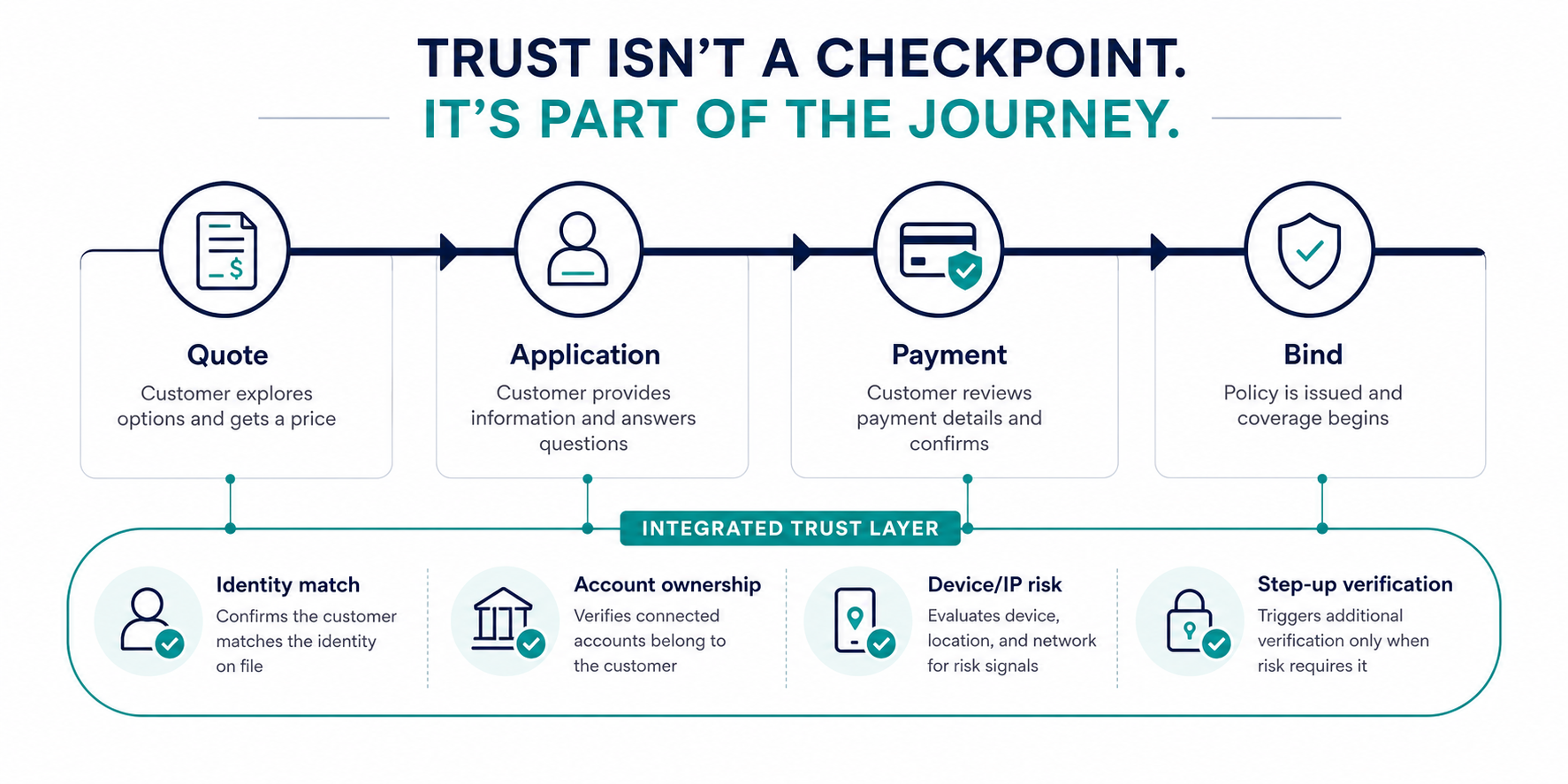

Fraud and verification belong inside the purchase flow

This is the piece I think many insurance carriers still underestimate.

Plaid's Identity product is built to verify account ownership and match account-holder information with the person going through the flow. Plaid's Identity Verification product adds documentary checks, device and IP risk, phone and email signals, and other anti-fraud capabilities.56

For insurance, this lands directly in the funnel.

Carriers have spent years thinking about acquisition, quote UX, page speed, and form optimization. Fair enough. But the bind flow in many categories still feels like it was designed for an era when the customer had low expectations and even lower leverage.

That era is ending.

If the front end of the journey becomes more intelligent, the back end has to become more trustworthy and more seamless at the same time. Identity checks can no longer feel bolted on. Account ownership confirmation cannot show up as a random interruption. Fraud prevention cannot rely on wrecking conversion and calling it discipline.

The next policy purchase flow has to reduce friction for legitimate users while raising assurance when a session actually deserves scrutiny.

That is product design as much as risk management.

We have seen pieces of this movie before

Two older references are useful here because they show the direction of travel.

Thaler saw the machine-readable version of this coming

In 2012, Richard Thaler argued that mortgage shopping would improve once disclosures were standardized and machine-readable enough for software to compare them properly.7

His insight was straightforward and still underappreciated.

A lot of consumer financial products are expensive in ways that are hard to parse. Once software can read the product cleanly, a lot of the old informational edge starts to leak away.

Plaid is not doing mortgages. It is building something broader: the conditions for machine-assisted financial decisioning at the consumer layer.

Goolsbee showed what happens when search costs fall in life insurance

Jeffrey Brown and Austan Goolsbee found that internet comparison shopping lowered term life insurance prices materially in the 1990s. Their NBER work showed that increased internet usage reduced prices for covered life insurance products, with estimated overall declines in the 8 to 15 percent range.8

That was the search-cost story.

The internet made comparison easier.

Agents will make comparison, decisioning, and follow-through easier.

That is a much bigger change.

Search still required initiative. Agents compress initiative.

Insurance carriers should read this as a market-structure change, not a UI trend.

Insurance does not get a pass here

The insurance industry has one extra complication.

Banking products often have cleaner direct data relationships and more obvious financial workflows. Insurance journeys are messier. They span partner sites, embedded flows, chat interfaces, quote engines, call centers, follow-up channels, payment pages, and bind systems that rarely feel like one coherent experience.

That fragmentation used to protect incumbents.

Now it is becoming a liability.

If consumers start in ChatGPT, ask clarifying questions there, get routed into a quote flow, call in for reassurance, and later return from SMS or email to complete purchase, the carrier cannot keep pretending the funnel begins on its own landing page.

That assumption is already out of date.

What matters now is preserving context, trust, and momentum across the whole journey.

A lot of carriers are still behind on that shift.

They are still optimizing for a world where the customer is under-informed and locally captive.

The next world belongs to the customer who arrives better briefed than the carrier expected.

What carriers should do with this

Consumers are becoming more empowered before they ever hit your site.

The old playbook is aging badly.

It assumed you could buy traffic, tune the web funnel, personalize the landing page, reduce page load, collect an application, and hope nothing broke before bind.

The next playbook starts with a different assumption: the customer may already have context, may arrive from an agent, and may move across multiple surfaces before purchase. Every handoff now matters.

Three design shifts for carriers

- Rethink the starting point. Your website is no longer guaranteed to be the beginning of the journey.

- Build for context portability. Customers should not have to restart the story every time the surface changes.

- Treat verification as experience design. Trust should feel embedded, not punitive.

What matters now

Plaid's announcement matters because it shows how quickly the market shifts once data access, semantic understanding, permissions, and verification start working together in the same stack.

Insurance carriers do not need another AI headline. They need to redesign around a customer who is more informed, more assisted, and less tolerant of broken handoffs than the customer their current funnel was built for.

The advantage will go to carriers that build for the empowered buyer on the other side of the click.

Notes and sources

- Plaid, “What ChatGPT's new experience signals for digital finance,” May 15, 2026. plaid.com/blog/chatgpt-personal-finance-plaid/

- Tyler Griffin, “The two paths of AI-enabled fintech,” July 28, 2025. loadhigh.jtylergriffin.com/the-two-paths-of-ai-enabled-fintech/

- Plaid Docs, “Payroll Income.” plaid.com/docs/income/payroll-income/

- Plaid Docs, “Transactions.” plaid.com/docs/transactions/

- Plaid Docs, “Identity.” plaid.com/docs/identity/

- Plaid Docs, “Identity Verification.” plaid.com/docs/identity-verification/

- Richard H. Thaler, “A Chance to Make Mortgage Shopping Easier,” New York Times, Aug. 18, 2012. consumerfinancemonitor.com/…/mortgage-shopping-ma.pdf

- Jeffrey R. Brown and Austan Goolsbee, “Does the Internet Make Markets More Competitive? Evidence from the Life Insurance Industry,” NBER Working Paper 7996 / Journal of Political Economy (2002). nber.org/papers/w7996